How to Prepare Your Records and Make the Most of End of Financial Year Purchases

Table of Contents

Key takeaways

- Start your EOFY bookkeeping early — don’t wait until June to reconcile.

- A bookkeeper organises and reconciles your records; an accountant gives tax advice.

- Reconcile bank accounts, payroll, leave balances and your asset register before 30 June.

- Plan EOFY purchases against cash flow — don’t buy just to spend.

- Payday Super starts 1 July 2026 — contributions must reach the fund within 7 business days of each pay run.

Every year, Australian business owners search for advice on how to get ready for the end of the financial year (EOFY). At the same time, many owners are still frantically trying to reconcile their books and find missing receipts.

As we are a Sunshine Coast bookkeeper based in Birtinya, we can’t give you tax advice, but we can help you get your records in order, so you can meet your obligations and make informed purchasing decisions before 30 June, 2026.

What are EOFY bookkeeping essentials and why they matter

EOFY bookkeeping is the process of organising, reviewing and finalising your business records before the end of the financial year. It includes gathering invoices and receipts, reconciling bank accounts, checking that your payroll data is accurate and ensuring your accounting software reflects every transaction.

Preparing your books early helps you avoid costly mistakes and gives your accountant a clear, accurate picture when it’s time to lodge your return. The Australian Taxation Office (ATO) recommends that businesses keep complete records of all transactions, including cash and electronic payments, and store them in a secure, organised system.

Unlike an accountant, a bookkeeper’s role is to maintain and reconcile your day-to-day financial records rather than providing tax advice or lodgements. We make sure your transactions are coded correctly, your payroll is up to date and your accounts balance.

This foundation allows your accountant to efficiently prepare your tax return, claim deductions and ensure compliance. Clear books also help you identify opportunities, such as whether you have room in your budget for an EOFY purchase or if you need to conserve cash for upcoming liabilities.

Key benefits of preparing your records early

Save time and reduce stress

When your records are organised throughout the year, you’re not scrambling for paperwork in June. A well‑structured system means fewer last‑minute calls to suppliers or searches through email threads.

Accurate financial insights

Clean books give you up-to-date profit and loss, cash-flow and balance-sheet reports so you know exactly where you stand. These insights help you decide whether an EOFY purchase, such as new software or equipment, is financially sensible.

Compliance and audit readiness

Having accurate records backed by valid receipts means you’re ready if the ATO asks for evidence. The ATO notes that good record keeping helps you substantiate claims and avoid penalties.

Smoother handover to your accountant

When your transactions are already reconciled and coded correctly, your accountant can focus on advisory work instead of fixing errors.

“When your records are organised throughout the year, you’re not scrambling for paperwork in June.”

Who this guide is for and when to use it

This guide is for sole traders and small‑business owners who:

- Pay employees or contractors and need to ensure payroll records are correct.

- Are planning to invest in equipment, software or vehicles at EOFY and want to organise these purchases efficiently.

- Operate in sectors with seasonal income, such as hospitality, tourism or trades, where cash‑flow timing matters.

- Want clear books to hand over to their accountant without needing tax advice from a bookkeeper.

- Are based in Birtinya, Caloundra, Maroochydore, Buderim, Noosa, or elsewhere on the Sunshine Coast and want bookkeeping records ready before EOFY.

If you’re wondering whether to claim specific deductions, speak with a registered tax agent or your accountant. A bookkeeper can prepare your records but cannot advise on tax strategies.

How to get your books ready for EOFY

Whether you work with a bookkeeper remotely or prefer local bookkeeping support across Birtinya, Caloundra, Maroochydore, Buderim or Noosa, the process starts with clean, complete records.

Gather and organise documentation

Collect all receipts and invoices for purchases, sales and expenses. Use a cloud‑based app or your accounting software’s mobile app to scan and attach receipts as you receive them. The ATO’s guide to record keeping provides examples of acceptable evidence and how long to keep it.

Download bank and credit‑card statements and reconcile them against your accounting software to ensure no transactions are missing or duplicated.

Check that all supplier invoices are entered and that you’ve received payment for outstanding sales. Follow up on overdue invoices before 30 June so that your revenue figures are accurate.

Review and reconcile accounts

Match every transaction in your accounting software with bank statements and cash receipts. Investigate discrepancies and correct any coding errors.

When it comes to payroll, verify employee details (names, TFNs, addresses, employment status and termination dates) and reconcile gross wages, PAYG withholding, allowances and salary‑sacrifice amounts.

Check that leave balances are accurate and that superannuation contributions have been paid on time. With Payday Super starting 1 July 2026, contributions will need to reach the fund within seven business days, review your process now.

Ensure your asset register lists the correct purchase dates and values. Update depreciation schedules and verify that loan balances agree with lender statements.

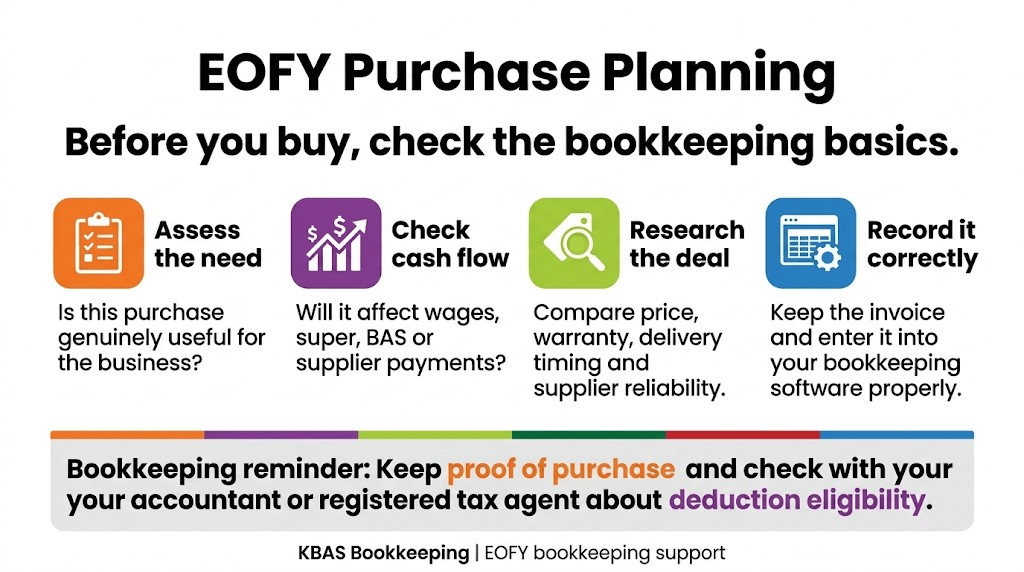

Audit your purchases and plan EOFY spending

During May and June, searches for office equipment, business software and company vehicles spike, indicating that many businesses are considering year‑end purchases. Before you join the rush:

- Assess your needs: Make a list of equipment or tools that genuinely support your business, such as upgraded laptops, new accounting software or vehicles for staff. Don’t buy simply to “use up your budget”; ensure the asset improves productivity or efficiency.

- Check cash‑flow forecasts: Create or update a cash‑flow forecast that includes the cost of the purchase and any financing repayments. Since super payments will soon coincide with pay runs, factor these in.

- Research deals: Look for EOFY sales from reputable suppliers. Sites like CHOICE Australia often publish round‑ups of sales events, and suppliers frequently advertise deals on their own websites. If a purchase qualifies for the government’s instant asset write‑off, discuss eligibility with your accountant.

- Record the purchase correctly: Once you decide to buy, keep proof of purchase and enter the transaction into your software. Categorise it as a fixed asset, not an expense, so depreciation can be applied correctly later.

“Don’t buy simply to ‘use up your budget’ — ensure the asset improves productivity or efficiency.”

Before you buy at EOFY check the bookkeeping basics

Avoid common mistakes

If you can’t find a receipt, ask the supplier for a copy or check your email. The ATO requires evidence for claims.

Coding a capital purchase as an expense or misclassifying wages as contractor payments can distort your profit and lead to compliance issues, so watch out for incorrect coding.

Ensure personal purchases are not recorded in your business accounts; maintain separate accounts to avoid confusion.

Don’t leave it to the last minute. Starting your EOFY preparation in June leaves little time to fix errors or follow up on missing documents. A rolling monthly reconciliation makes June’s tasks much easier.

Tools and technology

Platforms like Xero, QuickBooks Online or MYOB allow you to link bank feeds, automate invoicing and reconcile transactions quickly. They also integrate with payroll systems and receipt‑capture apps.

Tools such as Hubdoc or Dext extract data from receipts and invoices and attach them to transactions in your accounting software.

If you manage jobs or projects, apps like Trello or Asana can help you track expenses by project and attach receipts for easier reconciliation.

Local considerations

Businesses across the Sunshine Coast, including Birtinya, Caloundra, Maroochydore, Buderim and Noosa, often experience seasonal revenue swings and rely on casual staff. Hospitality and tourism operators, for example, may generate most of their revenue during summer and school holidays. When EOFY coincides with a quieter trading period, large purchases can strain cash flow if not planned carefully.

Conversely, trades and allied health services often see steady demand year‑round but need to juggle payroll and super obligations along with supplier payments. The upcoming Payday Super rules will add pressure, as super must be paid with each pay run rather than quarterly.

“When EOFY coincides with a quieter trading period, large purchases can strain cash flow if not planned carefully.”

By reviewing your books early and forecasting cash flow, you can decide whether to invest in new equipment or software now or wait until cash flow is stronger.

The bottom line

EOFY doesn’t have to be a scramble. Preparing your books early means you can make informed purchasing decisions, avoid common errors and hand over accurate data to your accountant. With Payday Super on the horizon and search interest in EOFY sales rising, now is the time to get organised, update your cash‑flow forecasts and double‑check your payroll records.

If you need help reconciling your accounts, implementing cloud-based tools or preparing your payroll for the new super rules, KBAS Bookkeeping can support your business from Birtinya across the Sunshine Coast, including Caloundra, Maroochydore, Buderim and Noosa.

FAQs

Q: What documents should I keep for EOFY?

A: Keep all invoices, receipts, bank statements, payroll summaries and any contracts related to purchases or services. The ATO’s record‑keeping guidelines specify that evidence must be kept for at least five years after the end of the financial year.

Q: When should I start preparing my books?

A: Ideally you should reconcile and review your accounts every month. Starting in late May gives you time to fix any issues before 30 June.

Q: How long do I need to retain records?

A: Generally, businesses must keep records for at least five years, though some documents (such as those relating to capital gains) may need to be kept longer. Consult the ATO or your accountant for specific requirements.

Q: What are common mistakes in EOFY record‑keeping?

A: Common errors include misclassifying assets, failing to reconcile accounts before finalising payroll, and omitting salary‑sacrifice or super contributions. Leaving these errors unresolved can delay your accountant and cause compliance issues.

Q: Should I make large purchases before EOFY?

A: Many businesses use EOFY sales to upgrade equipment or software. However, whether a purchase is beneficial depends on your cash flow and business needs. Speak with your accountant about potential tax implications; a bookkeeper can help ensure the purchase is recorded correctly.

Q: How can a bookkeeper help with EOFY preparation?

A: A bookkeeper maintains accurate day‑to‑day records, reconciles accounts, manages payroll and ensures your data is ready for your accountant. We can also help you implement systems that capture receipts and automate reconciliation.

Q: What’s the difference between a bookkeeper and an accountant?

A: Bookkeepers focus on recording and maintaining financial transactions, while accountants analyse that data to provide tax advice and prepare returns. Your bookkeeper ensures the information your accountant uses is accurate and up to date.

Q: Do I need to lodge payroll summaries?

A: Under Single Touch Payroll (STP), payment summaries have largely been replaced by STP finalisation. Employers must finalise payroll data by 14 July each year and employees access their income statement via myGov. Check with your accountant to confirm any exceptions.

Q: Do I need to be based in Birtinya to work with KBAS Bookkeeping?

A: No. KBAS Bookkeeping is based in Birtinya and supports businesses across the Sunshine Coast, including Caloundra, Maroochydore, Buderim and Noosa. Many bookkeeping tasks can be managed remotely, making it easier to keep your records up to date without needing to visit an office.